Disclosure regarding our editorial content standards

When rifling through your wallet, how many of the iconic men on the bills can you identify at random? You likely know that George Washington is on the $1 bill, and Benjamin Franklin graces the front of the $100 bill. But how about some lesser-known bills, like the $50 one?

Financial literacy is an important skill to be taught early on. Knowing skills like budgeting, how to pay your credit card bill and even how to identify who’s on the bills you’re spending are all key to ensure you’re a well-informed consumer. However, many people don’t receive the necessary amount of financial education needed to ensure they’re smart shoppers, which could come back around to bite them where it hurts—namely, their wallet or credit.

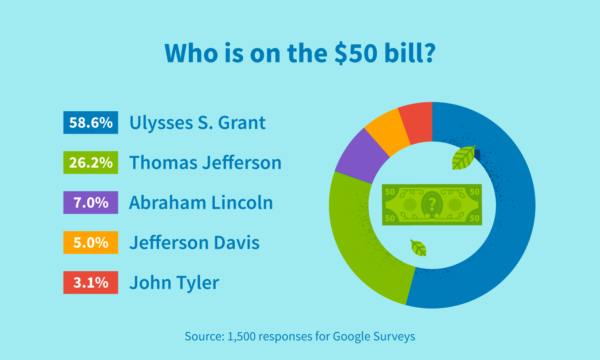

Who is on the $50 bill?

In a survey asking who was on the $50 bill, 41 percent of 1,500 respondents misidentified who was on it, showing that many consumers are spending their money without being educated on what their currency means.

Union Gen. Ulysses S. Grant graces the front of the $50 bill, which 58.6 percent of survey respondents guessed correctly. However, there were a variety of different guesses for the remaining 41.4 percent of respondents, which were as follows:

- Thomas Jefferson: 26.2 percent

- Abraham Lincoln: 7 percent

- Jefferson Davis: 5 percent

- John Tyler: 3.1 percent

Though all of the guesses were United States presidents, they encompassed over 100 years’ worth of presidential terms. Grant, who served as president of the United States from 1869 to 1877, has been on the front of the $50 bill issued by the United States Department of the Treasury since 1914.

There have been four different famous men on the front of the bill in its history. Since its creation in 1861, Alexander Hamilton, Henry Clay, George Washington and Benjamin Franklin have graced the front of the bill.

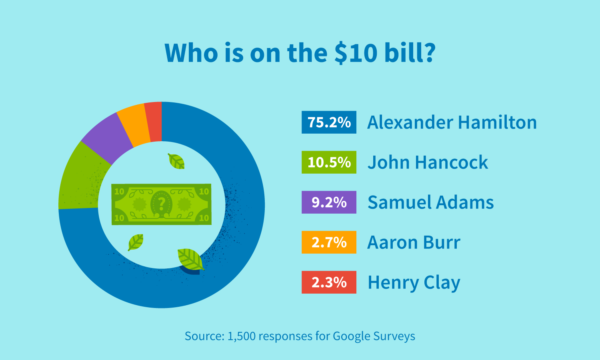

Who is on the $10 bill?

Though 40 percent of survey participants were unfamiliar with who was on the $50 bill, there was one bill they could easily identify: the $10 bill. Seventy-five percent of the surveyed population was able to correctly guess which Founding Father was on the front of the $10 bill: Alexander Hamilton.

The remaining 24.7 percent of respondents guessed as follows:

- John Hancock: 10.5 percent

- Samuel Adams: 9.2 percent

- Aaron Burr: 2.7 percent

- Henry Clay: 2.3 percent

Hamilton, who served as the first secretary of the United States Treasury from 1789 to 1795, has actually appeared on his respective bill for a shorter amount of time than Grant on the $50 bill. Hamilton appeared on the $10 bill for the first time in 1929, meaning Grant on the $50 bill has 15 years over Hamilton—but is lesser known than his Founding Father counterpart.

However, Hamilton has something on Grant other than time: notoriety, in the form of a smash Broadway musical about his life and accomplishments. The “10-dollar Founding Father,” as he is referred to in the opening line of the musical, has reentered popularity in large part due to the show.

Though it’s not necessary to be a walking trivia book of facts about your currency, it’s still important to be informed on what (and who) is in your wallet. These skills are all part of being financially literate, or knowing how to use different types of financial skills.

Other facts about American currency you probably didn’t know

Though you may be able to tell that George Washington is on the front of the $1 bill and John F. Kennedy’s profile is on the 50-cent coin, but what other information do you know about the currency you interact with every day?

Find out more fun facts about the dollars and coins you use on a daily basis below.

1. A different Washington was also used on a dollar.

Martha Washington was printed on the $1 silver certificate, first based on her official portrait and then with her husband, George. The last printing featuring America’s original first lady ran in 1896, with silver certificates ending their run as currency in 1956.

To this day, only two women have been memorialized on American currency: Martha Washington and Pocahontas.

2. Paper money isn’t actually made of paper.

Though bills are referred to as “paper money,” that doesn’t accurately represent what they’re made of. They’re actually made of 75 percent cotton and 25 percent linen, and are shipped in sheets of 20,000 to the U.S. Treasury’s Bureau of Engraving and Printing to be printed.

The various ink colors used to print the iconic figures on your money are specially mixed by the bureau, using a secret recipe for security reasons.

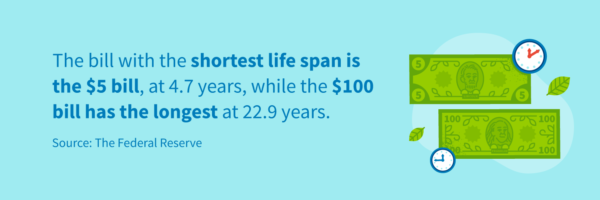

3. Bills fall out of circulation frequently.

How often do bills get retired or fall out of circulation? The $5 bill has the shortest life span, at an estimated 4.7 years, with the $100 bill claiming the longest, at 22.9 years. The life span of other bills are as follows:

- $5 bill: 4.7 years

- $10 bill: 5.3 years

- $1 bill: 6.6 years

- $20 bill 7.8 years

- $50 bill: 12.2 years

- $100 bill: 22.9 years

4. Torn bill? No problem.

If you have a partially torn bill in your wallet you’ve been nervous to use, this one’s for you—as long as 75 percent of a bill is intact, you can exchange it for a new one. If the bill is torn in half, it can be used as long as the serial numbers on the front and back of the bill match.

If your bill is mangled beyond repair, you can send it over to the Bureau of Engraving and Printing’s Mutilated Currency Division, who will review and often replace your bills. This entity deals with approximately 30,000 claims annually.

5. The largest bill ever printed was worth hundreds of thousands.

The $100 bill may seem big to some, but how about $100,00? That bill holds the record for the largest bill denomination ever printed as official U.S. currency. This was printed as a $100,000 Series 1934 Gold Certificate, featuring the bust of President Woodrow Wilson.

These bills were used only December 1934 through January 1935, and were mainly used in official transactions between different branches of the Federal Reserve.

6. Look closely for 13.

Much of the symbolism on the $1 bill represents America in its youth, including a number of nods to the 13 original colonies. There are 13 steps on the pyramid featured on the back of the dollar bill, 13 arrows in the eagle’s talons and 13 stars on the Great Seal.

The importance of financial literacy

Knowing not only how to manage money, but how to identify it and what its value is are the building blocks necessary to be successful with your finances. Once you have these skills down, you will likely feel more confident making well-informed financial decisions, like distinguishing between needs and wants.

There are a few ways you can up your financial literacy at home:

- Know your currency. Familiarize yourself with the currency you use on a regular basis. This includes both the value of your bills and coins, as well as who’s on them.

- Budget each month. If budgeting on paper isn’t for you, try using online budgeting calculators, apps, cash envelopes or another method that works best for you and your unique situation. Budgeting is highly personal and is dependent on a number of factors, so don’t be afraid to try different budgeting methods until you find the one that works best for you.

- Try investing. Starting small with investments is key, as you don’t want to put all of your eggs (or money) in one basket only for the investment to tank. Using an investment app or service may be helpful here.

- Pay off your loans and debt. Examine and begin paying off any debt you may have, including student loans, personal loans, credit card debt, home mortgages and any other loans or debt you’ve incurred. This will help your debt-to-income (DTI) ratio, which makes you eligible for some better financing options in the future.

- Work on your personal money management. Don’t be afraid to ask for help if you need help with personal money management. Talk to a trusted friend who’s great at budgeting, a counselor at a bank or a team of credit repair professionals.

Knowing your currency and bettering your financial literacy can seem intimidating, but it doesn’t have to be. Doing what you can to increase your financial knowledge will make you a better consumer, resulting in a positive effect on your credit.

This study was conducted for CreditRepair.com using Google Consumer Surveys and interpreted by Siege Media. The sample consisted of no less than 1,500 completed responses per question. Post-stratification weighting has been applied to ensure an accurate and reliable representation of the total population. This survey was conducted in April 2021.