Disclosure regarding our editorial content standards.

If you have an old outstanding debt in Florida, you might be worried that your creditor or a collection agency will come after you. However, the statute of limitations plays a significant role in debt collection. In most cases, the maximum statute of limitations for Florida debt is five years, although some debts only have a statute of limitations of four. This means a creditor only has four to five years to sue you for the debt you owe.

What is the statute of limitations?

A statute of limitations is a law that sets a maximum time during which a party can begin legal proceedings, such as a lawsuit, against another party. The statute of limitations typically starts from the day the event occurred. There’s a statute of limitations for various offenses, including failure to pay debts. Each state can set its own statute of limitations on debt collection lawsuits.

Generally speaking, the statute of limitations exists because evidence and the likelihood of a strong case deteriorate as time goes on. The law doesn’t want to allow or reward people for inaction, so individuals are given a reasonable period when they can bring forward legal action.

What does time-barred mean?

After the statute of limitations passes, debt becomes time-barred. When someone refers to “time-barred debt,” it means money was borrowed and never repaid but is no longer legally collectible because the statute of limitations has passed.

What does tolled mean?

Tolled is also known as “extending the statute.” Debt can be tolled when a consumer takes an action that legally allows the statute of limitations to be extended.

For example, let’s say an individual ignores all communication attempts from their creditor and moves to another state because they know there’s only one year left before the statute of limitations is up. In this case, the creditor can take action to toll the debt, and if the person ever moves back, the creditor gets that year back on their statute.

In some states, debt can be tolled if the borrower admits they know about the debt or makes a partial payment. For this reason, consumers must be cautious when dealing with creditors.

Note that tolling a statute of limitations only applies to debts with a written contract, such as a loan or credit card agreement.

How does the statute of limitations work with debt in collections?

If your debt is in collections, whoever currently owns the debt can file a lawsuit against you as long as the statute of limitations hasn’t passed. This means that even if your original creditor has written off the debt and passed it on to a collection agency, that agency can still take legal action within the allowable five-year statute.

What if the statute of limitations has passed?

Once the statute of limitations has passed, a creditor can no longer take legal action against you. If they try to, you can file a motion to dismiss the case. The court won’t have your account records, so the responsibility will be on you to prove the statute of limitations has passed. Once you can show that, your case will be dismissed.

Note that while the creditors can’t take legal action, they can still try to contact you for collection on the account, and it can still appear on your credit report.

Be careful in engaging with your creditors, as you can accidentally reset or “toll” the statute of limitations. Don’t try to communicate with them about dropping the lawsuit, offering partial payments or acknowledging the debt, as this can have undesired consequences.

What is the Florida law on the statute of limitations?

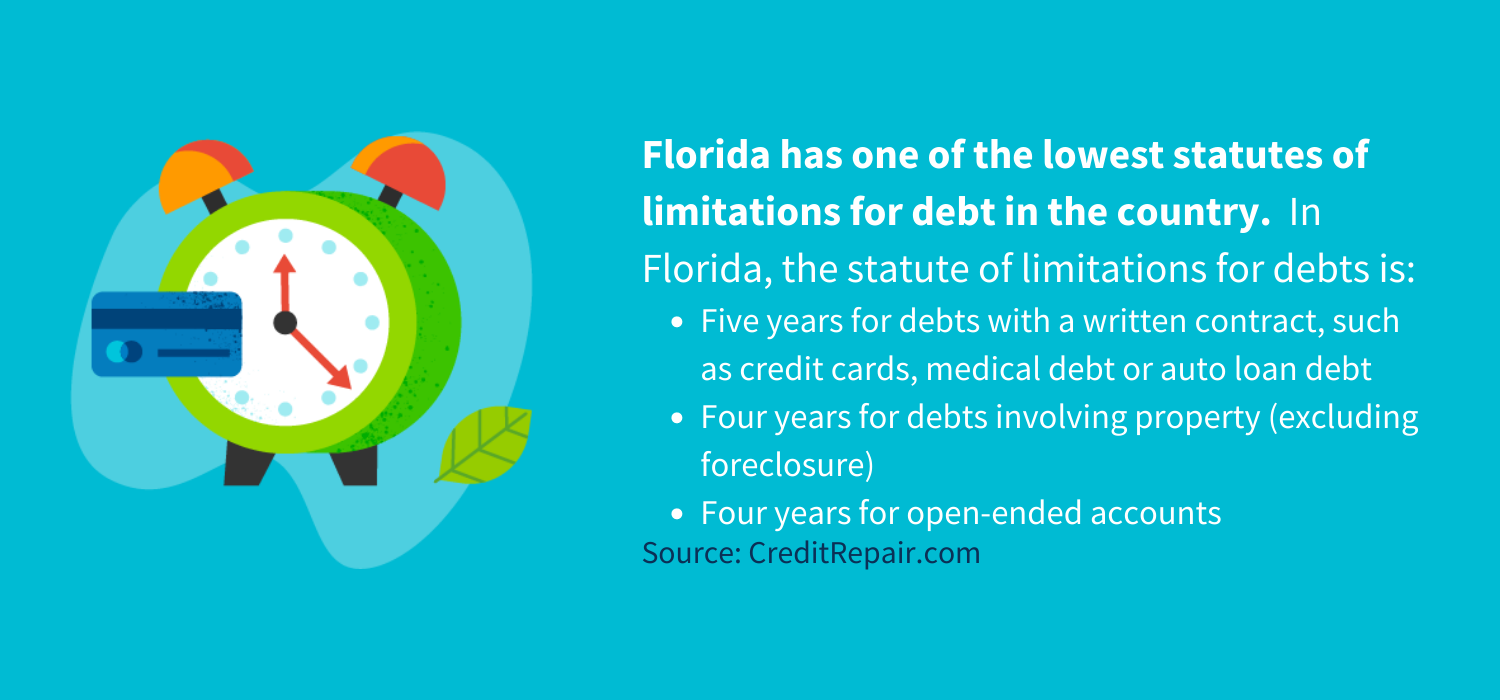

Florida has one of the lowest statutes of limitations for debt in the country. The majority of states have a statute of six years. In Florida, the statute of limitations for debts is:

- Five years for debts with a written contract, such as credit cards, medical debt or auto loan debt

- Four years for debts involving property (excluding foreclosure)

- Four years for open-ended accounts

The statute of limitations typically starts from the last activity on the account, whether that’s a payment, a charge or a credit.

Note that the statute of limitations only applies to legal action for consumer debts in Florida. This means a collection agency or creditor can continue to attempt to collect on the debt even past the statute—they just can’t file a lawsuit.

Additionally, in Florida, making a partial payment on a debt will toll the debt, resetting the statute of limitations.

One important distinction is that if a judgment has been entered against you in court, the statute of limitations for Florida debt expands to 20 years and will continue to accrue interest until it’s paid. In some cases, creditors can have certain assets seized or wages garnished to recover what’s owed.

What debt falls under the statute of limitations?

The debts that fall under the statute of limitations include:

- Credit cards

- Personal loans

- Mortgages

- Auto loans

- Private student loans

- Medical debt

- State tax debt

Some debts have no statute of limitations, including federal student loans and unpaid child support.

What should you do if you are being sued for old debt?

If you’re being sued for old debt in Florida, the first step is to figure out the date of the last activity on the account. Depending on the type of debt, you know you have a four- or five-year statute of limitations. If you feel confident that the statute of limitations has passed, don’t speak with the creditor and don’t make any payments. Instead, hire an attorney to review your case and file a motion to dismiss the lawsuit.

On the other hand, if you’re being sued for an old debt but the statute of limitations hasn’t passed, you’ll need to come up with a plan. If the debt is accurate, the judge will likely side with the creditor. As a result, you might find that you receive a judgment, such as a wage garnishment or a lien put on your property. The total amount you’ll owe may cover the original debt, as well as any interest, fees and potentially attorney fees.

It’s highly recommended that you show up to court and try to defend yourself, even if you know the debt is accurate. Showing up to court increases the chances the judge will give you a lighter penalty.

What should you do if you have debt in collections that hasn’t passed the statute of limitations?

Let’s say you have debt in collections that hasn’t passed the statute of limitations but you haven’t been served a lawsuit, either. The important thing here is not to wait around and hope the creditor doesn’t take legal action against you. Instead, it’s essential to communicate with the creditor and try to rectify the situation.

If the debt is accurate, you have a couple of options:

- If you have the cash available, offer a one-time lump-sum payment for less than you owe. In exchange for this payment, you’ll ask them to consider the debt settled, and you may even ask them to remove the debt from your credit report (pay for delete letter). If you pursue this option, get everything in writing so you have proof of the promises made.

- If you don’t have the cash for a lump-sum payment, reach out and ask your creditor if you can set up a monthly payment plan. This can prevent you from being taken to court as long as the creditor agrees and you stick to your payments. Again, get everything in writing.

If the debt is inaccurate, you’ll want to dispute to potentially have it removed from your credit report and stops impacting your credit score. You have the legal right to a fair and accurate credit report, and debt collectors can’t come after you for inaccurate debts.

It’s possible to file a dispute independently with the credit bureaus, but many people choose to get professional help in this area. For example, CreditRepair.com members saw over 8.2 million removals on their credit reports since 2012.

There’s no reason you have to do this alone—let our credit repair advocates help you today.

Note: The information provided on CreditRepair.com does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only.

Questions about credit repair?

Chat with an expert: 1-800-255-0263